Taxes and Pensions

Income Tax / 所得税 (shotokuzei)

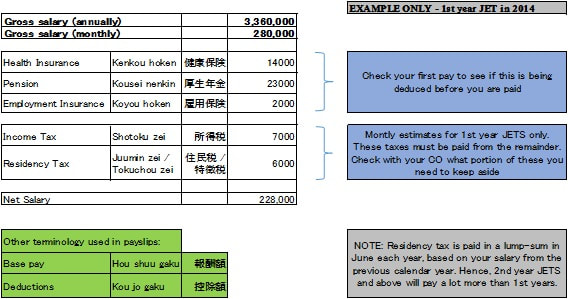

This is income tax directly deducted from your salary each month and paid to the central government. This will be handled entirely by your employer, but please check to make sure it is being deducted every month. It is worth noting that the amount of income tax may vary each month (sometimes quite considerably) as tax over certain periods is increased/decreased to account for under/over-payments in prior periods and miscalculations. Depending on your home country, you may be required to pay income tax in your home country.

Residency Tax / 住民税 (juminzei)

This is the tax you pay to the governments of the Prefecture and Municipality you reside in. For example, a JET living in Gifu City will have their residency tax split between Gifu Prefecture and Gifu City. You should be aware of the following:

- Residency tax is calculated as a percentage of your income over the previous calendar year (i.e. January 1st – December 31st) but is paid for the financial year. For example, at the start of the 2018 financial year (May 2018), you will have an amount of tax to pay calculated based on your income in the previous calendar year (January 1st 2017 – December 31st 2017).

- As the tax is calculated based on the previous calendar year, this means that most JETs will have very little to pay for the first year on the programme. A JET arriving to Japan in August, never having had an income in Japan before, will have had no previous income until the start of the next calendar year, and for the next financial year will only have had the five months of income from August to December.

- Any new JETs who have been working in Japan directly prior to joining the JET Programme should be mindful that their residency tax might be considerably higher than that of JETs who are freshly arriving in Japan, even if they had previously been working on a tax-exempt basis.

- Your CO may or may not automatically deduct your tax. If not, you should be saving money each month for when the bill comes in June. Makes sure to ask your supervisor about this.

- Moving Prefectures/municipalities or leaving Japan can lead to a large residency tax bill which you will need to pay at once.

Tax Exemptions

In certain circumstances ALTs from certain countries may be eligible for up to two years of tax exemption. Tax exemptions are not available to CIRs. In general, tax exemptions are available to ALTs from the following countries:

France

Ireland

The Philippines

Ireland

The Philippines

JETs are strongly advised to research and be aware of any tax requirements their home countries may impose upon them. JETs from the United States in particular may be subject to strict requirements for reporting tax. Such arrangements are their own responsibility. PAs, while they may be able to informally offer advice or resources in certain circumstances, cannot generally be expected to advise on the requirements of countries other than Japan.

Pensions

As residents working in Japan, all JETs are obliged to pay contributions towards the Japanese National Pension scheme. This will be deducted by your Contracting Organization from your monthly salary. This might seem like a waste of money if you are not planning to retire in Japan, but you will be able to have refunded up to three years of pension contributions when you leave Japan.

US Tax Guide - Courtesy of Kumamoto JET

Thanks to Kumamoto JET there are comprehensive US Tax Guides to file for 1st year JETs and 2-5th year JETs.